The California Public Employees’ Retirement System is presenting its new “Total Portfolio Approach” (“TPA”) as a sophisticated modernization of pension investing. According to consultants and pension executives, TPA will make the fund more agile, more collaborative, and more focused on total-fund outcomes rather than rigid asset-class silos.

But beneath the polished institutional language lies a much simpler reality.

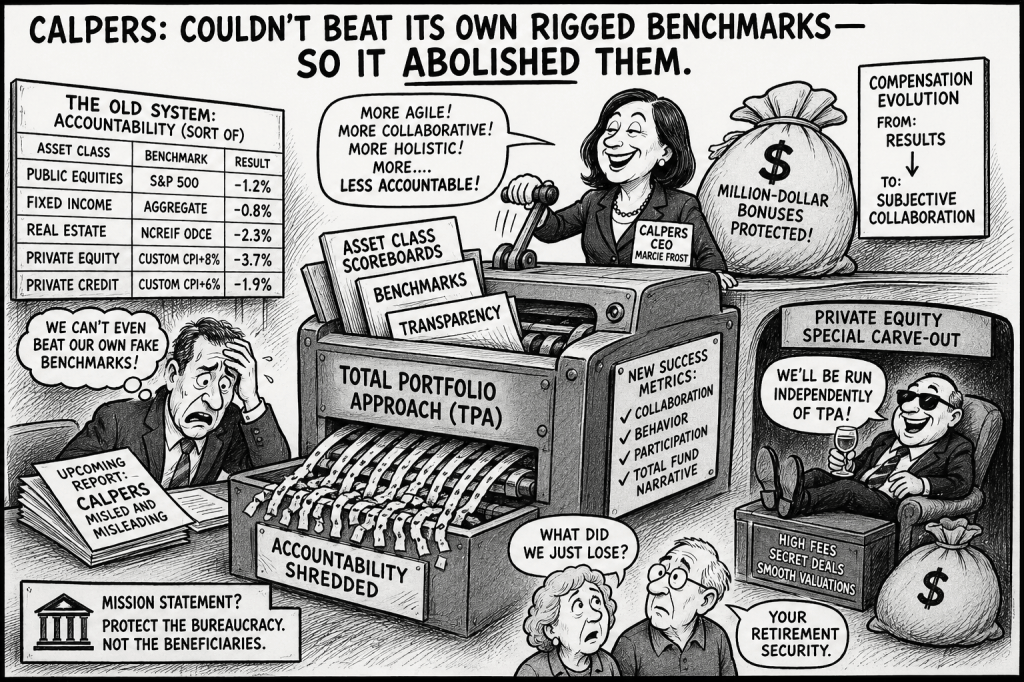

“CalPERS couldn’t beat its own rigged benchmarks — so it abolished them.”

TPA is primarily a governance and compensation restructuring mechanism designed to reduce transparency precisely when transparency is becoming most politically dangerous for CalPERS.

For years CalPERS relied on increasingly subjective and internally constructed benchmark systems to justify both mediocre performance and extraordinary compensation.

- custom policy benchmarks,

- CPI-plus hurdle rates,

- lagged private-market valuations,

- IRR-driven narratives,

- and consultant-designed comparisons that often lacked meaningful public-market equivalents.

Even with those advantages, long-term performance continued to lag simpler and cheaper public market alternatives. https://www.rpea.com/view/download.php/news/calpers-investigation-report

The problem for CalPERS is not merely investment performance. The problem is that the compensation structure depends on maintaining the appearance of alpha generation.

Today CalPERS has:

- multiple employees making over $1 million annually,

- dozens making over $500,000,

and a rapidly expanding investment bureaucracy whose compensation increasingly resembles Wall Street rather than public service. https://californiapolicycenter.org/calpers-pays-million-dollar-salaries-for-below-median-returns/

CEO Marcie Frost reportedly earns over $1.4 million per year despite lacking even a college degree.

The upcoming scrutiny surrounding private equity fees, hidden leverage, valuation smoothing, and benchmark manipulation threatens both the investment narrative and the compensation narrative simultaneously.

So the institution is changing the rules.

Not by reducing fees.

Not by simplifying the portfolio.

Not by increasing transparency.

Not by opening private equity agreements to public scrutiny.

Instead, CalPERS is eliminating many of the scoreboards themselves.

Under the traditional framework, each asset class had its own benchmark:

- public equities,

- fixed income,

- real estate,

- private equity,

- private credit.

The system was imperfect, but at least beneficiaries and watchdogs could attempt to isolate which programs were adding value and which were not.

TPA collapses those distinctions into a single “reference portfolio,” generally resembling a passive mix of global equities and bonds.

Once individual scoreboards disappear, accountability disappears with them.

A poorly performing private equity program can now be masked inside broader total-fund narratives. Excessive fees become harder to isolate. Hidden leverage becomes harder to evaluate. Valuation smoothing becomes more politically useful.

The institutional bureaucracy gains discretion while beneficiaries lose visibility.

This is not an accident.

The compensation changes surrounding TPA reveal the real purpose of the transition. CalPERS has openly discussed moving compensation away from transparent benchmark-based systems toward more subjective concepts such as:

- “cross-asset collaboration,”

- organizational behavior,

- and total-fund participation.

In practice this means:

when measurable performance becomes harder to defend, redefine success itself.

The shift from objective benchmarks to subjective collaboration is enormously important because subjective systems are easier to manipulate institutionally. If performance disappoints:

- broaden the metrics,

- increase managerial discretion,

- redefine outcomes,

- and reward “collaboration.”

This is not investment modernization.

It is bureaucratic self-protection.

The contradictions become even more revealing when private equity enters the discussion.

At PEI Nexus 2026, CalPERS CEO Marcie Frost reportedly stated that the private equity program “will be run independently of TPA.”

That admission effectively undermines the philosophical foundation of the entire project.

TPA was sold as:

- integrated governance,

- unified capital allocation,

- and total portfolio accountability.

Yet the single largest, most opaque, most fee-intensive asset class receives a carve-out from the discipline itself.

Why?

Because private equity has become the political and financial center of the modern pension ecosystem.

Private equity:

- generates enormous hidden fees,

- depends on subjective valuations,

- relies on confidential contracts,

- and produces the accounting smoothness necessary to sustain compensation narratives.

A truly transparent Total Portfolio Approach would force uncomfortable questions:

- Are the returns real?

- Are the valuations realistic?

- Are the diversification claims genuine?

- Are the fees justified?

- Are the benchmarks manipulated?

TPA helps blur those questions.

And when even TPA threatens to expose too much, private equity receives special insulation.

The result is a system where:

- public markets remain fully transparent and continuously priced,

- while private equity remains confidential, quarterly marked, politically protected, and partially exempt from the new governance structure itself.

That is not equal treatment under a total portfolio framework.

It is institutional asymmetry.

Supporters of TPA argue that the old asset-class structure prevented flexibility and slowed decision-making. There is some truth to that criticism. But replacing transparent benchmarks with broad total-fund narratives and subjective compensation metrics does not improve accountability.

It weakens it.

Public pensions already suffer from severe information asymmetry. Board members often depend heavily on consultants. Beneficiaries rarely see the underlying agreements. Journalists and watchdogs struggle to piece together fragmented disclosures.

In that environment, removing benchmark transparency does not empower beneficiaries.

It empowers the bureaucracy.

The pattern is familiar across financial institutions. When performance is strong, managers welcome scrutiny. When performance becomes difficult to defend, reporting structures become more complicated.

The Total Portfolio Approach fits that pattern almost perfectly.

At bottom, TPA is not primarily about portfolio construction.

It is about protecting a compensation and governance structure built around opaque private markets, subjective valuations, and increasingly discretionary definitions of success.

If private equity truly delivers superior risk-adjusted returns after fees, it should withstand transparent benchmarking and public scrutiny.

If it instead requires:

- secret contracts,

- benchmark redesign,

- subjective compensation,

- carve-outs from TPA,

- and diminished transparency,

then beneficiaries should begin asking a simple question:

Does this system exist primarily to protect retirees —

or to protect the investment bureaucracy itself?

TPA: The Wall Street Trick CalPERS Uses to Hide Underperformance and Protect Million-Dollar Bonuses

https://www.bloomberg.com/news/articles/2026-06-10/a-600-billion-experiment-kicks-off-at-calpers-pension-fund https://commonsense401kproject.com/2026/05/22/calpers-sets-its-own-excessive-pay-off-the-charts/

https://www.top1000funds.com/investor-profile/cio-monte-tarbox-charts-new-course-for-nyc-pension NYC skeptical of TPA