The crypto industry keeps insisting that regulation will somehow make crypto “safe” for retirement plans.

But the new PwC Global Crypto Regulation Report 2026 accidentally says the quiet part out loud again:

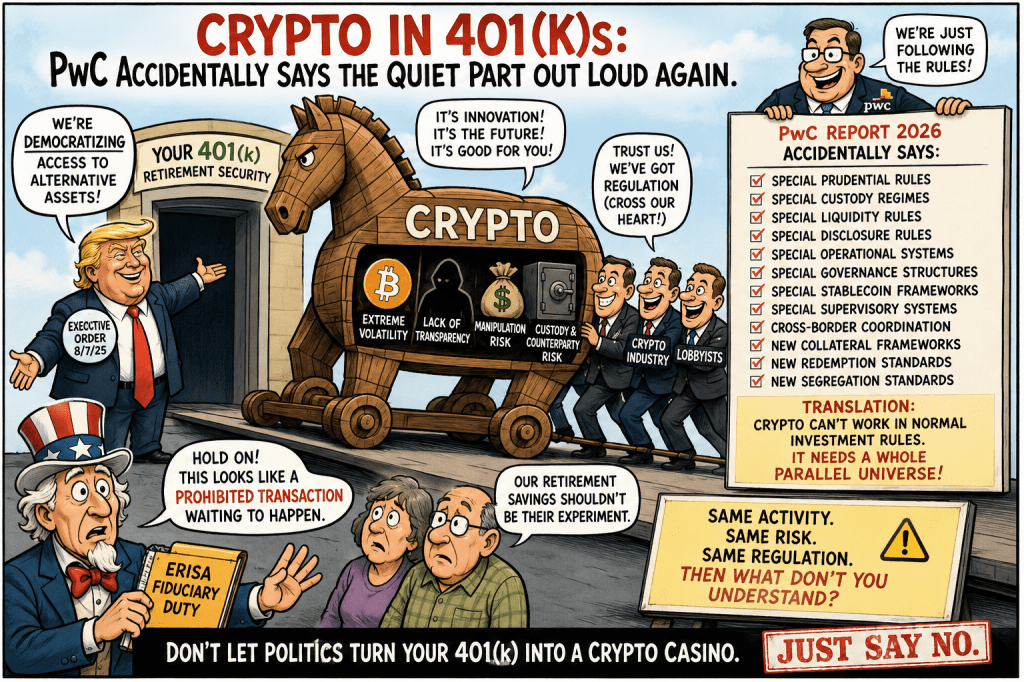

Crypto only works if you build an entirely separate legal, custody, governance, valuation, disclosure, liquidity, and operational framework around it.

That is not an argument for putting crypto in 401(k) plans.

It is the strongest argument against it.

The entire report reads less like a normal investment discussion and more like a manual for managing systemic instability.

PwC’s Real Message

PwC openly admits that crypto requires:

- special prudential rules

- special custody regimes

- special liquidity rules

- special disclosure rules

- special operational resilience systems

- special market conduct rules

- special governance structures

- special stablecoin reserve frameworks

- special supervisory systems

- cross-border enforcement coordination

- new collateral frameworks

- new redemption standards

- new segregation standards

In other words:

Crypto cannot survive inside normal securities law and normal fiduciary standards.

PwC says the industry is moving from “policy design to implementation” and that stablecoin, custody, and disclosure regimes are now becoming operational. That alone tells you the product itself is inherently unstable without constant regulatory intervention.

Traditional diversified mutual funds do not require a global emergency architecture to function.

Crypto does.

“Same Activity, Same Risk, Same Regulation”

The PwC report repeatedly cites the Financial Stability Board principle:

“same activity, same risk, same regulation.”

That phrase destroys much of the political sales pitch around crypto in 401(k) plans.

Because if crypto is truly subject to the same fiduciary standards as traditional retirement investments, it immediately runs into enormous ERISA problems:

- valuation uncertainty

- liquidity concerns

- custody risk

- counterparty risk

- operational risk

- conflicts of interest

- prohibited transaction exposure

- impossible benchmarking

- excessive spreads and fees

- market manipulation risk

- unstable collateral frameworks

The crypto industry wants the legitimacy of securities law while simultaneously arguing it should not be regulated like securities.

That contradiction sits at the center of the entire debate.

PwC Accidentally Admits Crypto Depends on Regulatory Arbitrage

One of the most revealing passages in the report warns that differing global frameworks create:

- “regulatory arbitrage”

- “localisation pressures”

- fragmented supervision

- inconsistent implementation

PwC openly admits that global implementation remains “incomplete and inconsistent” and warns about weak oversight and fragmented supervision.

That is not a retirement plan investment thesis.

That is a warning label.

ERISA fiduciaries are supposed to minimize conflicts, opacity, instability, and uncompensated risks.

Crypto multiplies all four.

Impossible Benchmarking

One of the core fiduciary problems with crypto is that there is no meaningful benchmark framework.

This is the exact same problem that exists with:

- private equity

- private credit

- annuity wrappers

- state-regulated CIT structures

- tokenized “alternative” products

Crypto pricing is fragmented across exchanges, jurisdictions, liquidity pools, stablecoin systems, and offshore entities.

Even the so-called “stable” part of crypto depends on reserve assumptions, redemption mechanics, and counterparty structures that regulators still cannot consistently supervise globally.

PwC admits stablecoin frameworks remain divergent worldwide.

Reserve rules differ.

Redemption standards differ.

Issuer rules differ.

Holding limits differ.

Cross-border access differs.

How exactly is a 401(k) fiduciary supposed to benchmark that against prudent public market investments?

The answer is simple:

They cannot.

Crypto Is Becoming the New Gateway Drug

The political strategy around crypto mirrors the exact same playbook used for annuities and private equity in retirement plans.

Step 1:

Claim “innovation.”

Step 2:

Promise “democratized access.”

Step 3:

Hide complexity behind wrappers.

Step 4:

Use brokerage windows, target-date funds, or CITs to bury the exposure.

Step 5:

Normalize higher fees, weaker disclosure, and lower transparency.

PwC essentially confirms this evolution by describing crypto as becoming integrated into:

- payments

- collateral systems

- banking infrastructure

- settlement rails

- tokenized deposits

- treasury operations

That means crypto exposure no longer stays isolated.

It migrates into the plumbing of retirement systems themselves.

Exactly what happened with:

- general account annuities

- synthetic products

- private credit

- target-date CITs

- insurance wrappers

Stablecoins Are Not “Stable”

PwC spends enormous effort discussing stablecoin regulation.

That alone should terrify fiduciaries.

If an investment product requires:

- reserve segregation rules

- redemption-at-par mandates

- stabilization mechanisms

- recovery and resolution planning

- prudential capital oversight

- liquidity management systems

then it is not remotely comparable to a normal diversified retirement investment.

Stablecoins increasingly resemble lightly regulated shadow banks operating through technology wrappers.

And retirement plans are now being asked to trust these systems with lifetime savings.

The Warren Letter Gets the Real Issue Right

Senator Elizabeth Warren’s January 2026 letter correctly highlights the central issue:

Crypto volatility, weak investor protections, lack of transparency, and potential manipulation are fundamentally incompatible with retirement security.

The letter points out that Bitcoin lost roughly 33% in six weeks, wiping out nearly $800 billion in value.

That is not retirement investing.

That is speculation.

And under ERISA, fiduciaries are not supposed to gamble with participant retirement savings simply because political pressure or industry lobbying demands it.

The Real Problem Is Structural

Crypto supporters keep arguing:

“Regulation will fix crypto.”

But the PwC report unintentionally shows the opposite.

The more regulation required to stabilize crypto, the more obvious it becomes that crypto itself creates the instability.

Normal retirement investments do not require:

- global enforcement coordination

- special reserve systems

- cross-border supervision

- tokenized collateral rules

- systemic redemption frameworks

- continuous prudential intervention

Crypto does.

That is why crypto in 401(k) plans increasingly looks less like innovation and more like another prohibited transaction ecosystem searching for a wrapper.

Just like:

- private equity

- private credit

- annuity contracts

- opaque CIT structures

The common thread is always the same:

Opacity creates spreads.

Spreads create profits.

And participants absorb the risk.

That is not democratization.

That is financial engineering.