The CFA Institute has diagnosed yesterday’s disease while today’s patient is dying from something entirely different.

By Chris Tobe, CFA, CAIA

The new CFA Institute Research Foundation monograph Investment Committees: Governance and Design Choices deserves praise. It is one of the best academic treatments of investment committee behavior I have read in years. It synthesizes decades of behavioral finance research into a thoughtful discussion of groupthink, status bias, anchoring, and decision-making “noise.” It even proposes an innovative idea: instead of allowing dominant personalities to steer committee discussions, require each committee member to independently submit portfolio recommendations anonymously before discussion begins. The committee’s decision would then reflect the average of those independent judgments rather than the loudest voice in the room. https://rpc.cfainstitute.org/sites/default/files/docs/research-reports/rf_scherer_investmentcommittees_online.pdf

Twenty years ago, this paper might have represented the cutting edge of institutional governance.

Today, however, it feels like a diagnosis of a disease that has largely disappeared.

The problem facing investment committees in 2026 is not that they are making honest mistakes. The problem is that many committees have stopped asking the questions that matter.

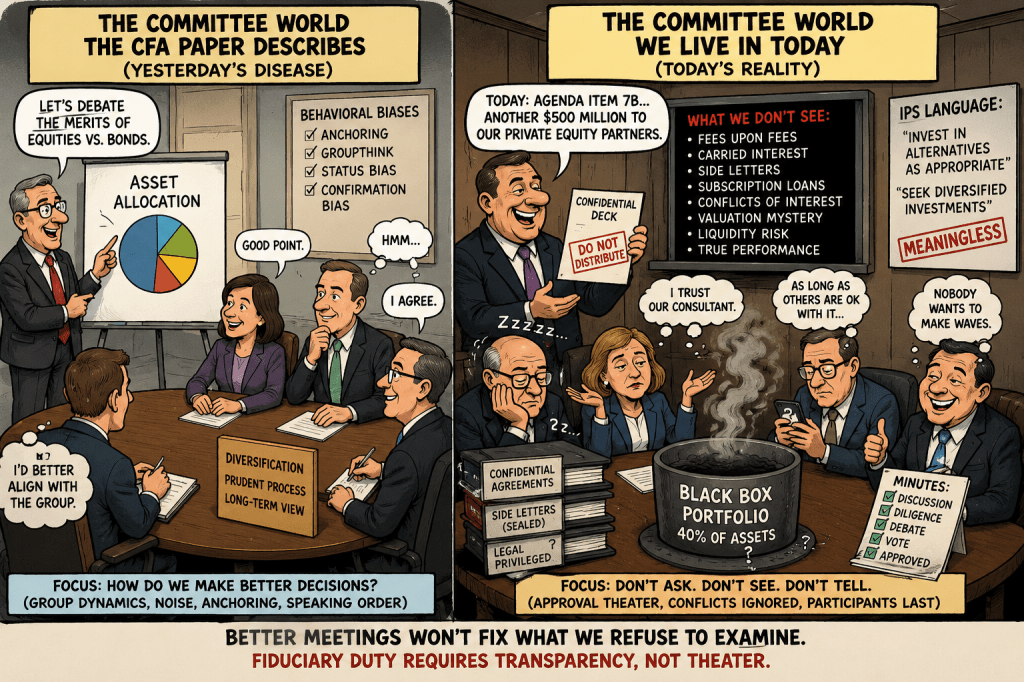

The World the CFA Paper Describes

The CFA paper assumes a traditional institutional investor. Committee members gather monthly. They review economic forecasts. They debate equity versus bonds. The CIO may dominate discussion. Members may anchor on the first opinion expressed. Groupthink can emerge.

Behavioral biases distort decisions. These are all real problems. The research on committee psychology is excellent, and the proposed reforms could improve many investment committees. But underlying the entire paper is one crucial assumption:

Committee members are honestly trying to maximize participant returns.

That assumption once described much of institutional investing. It increasingly does not especially in my world of U.S. Public Pensions and 401(k) plans.

The Investment Committee Has Changed

Over the last two decades, alternatives have fundamentally changed the role of investment committees especially in U.S. Public Pension Plans.

The traditional committee once allocated among:

- U.S. equities

- International equities

- Bonds

- Cash

Today many public pension committees spend nearly half their meetings discussing:

- private equity

- private credit

- hedge funds

- infrastructure

- real estate partnerships

- continuation funds

- GP-led restructurings

- insurance products

These are not transparent securities. They are contractual relationships.

And contracts create conflicts. The committee’s most important job is no longer deciding whether stocks should be 58% or 62% of the portfolio.

It is determining whether fiduciaries are entering relationships that participants cannot evaluate.

The Questions That Never Get Asked

After serving as an expert witness in ERISA litigation for more than a decade, and doing public pension reviews for over 2 decades, I have reviewed thousands of committee materials. I have served as a trustee of a $20 billion pension fund.

The missing discussions are remarkably consistent.

Committees rarely ask:

- How much are we really paying?

- Who receives every layer of compensation?

- What conflicts exist?

- How are these assets actually valued?

- What happens if liquidity disappears?

- Who benefits from secrecy?

- Why are these contracts unavailable for public review?

Instead, committees often spend hours debating issues around 1 of several hundred investments, and get just the consultants boiler plate presentations on the economy.

The CFA paper spends nearly eighty pages discussing committee dynamics. It spends almost no time discussing conflicts of interest. That omission illustrates how much institutional investing has changed.

The New Governance Failure

Behavioral finance remains important. But today’s governance failures are structural.

Increasingly, committees are approving investments whose economics cannot be independently verified. Consider private equity. Many public pensions now allocate 30% to 40% of assets to private markets.

Yet those investments frequently rely on:

- manager-supplied valuations

- confidential side letters

- confidential partnership agreements

- confidential fee arrangements

- confidential financing structures

In many cases even the Investment Committee members are not allowed to see these private equity contracts.

Ironically, many of these investments cannot satisfy the transparency principles long promoted by the CFA Institute’s own Global Investment Performance Standards (GIPS). When nearly half of a pension portfolio consists of assets that resist standardized performance verification, governance problems become far more serious than groupthink. They become problems of accountability.

Investment Policy Statements Have Become Hollow

This is where the CFA paper and modern ERISA litigation diverge. The paper assumes committees operate within robust Investment Policy Statements.

My public pension investigations and litigation experience suggests something different.

Many IPS documents have become increasingly vague precisely where specificity matters most.

Instead of requiring fiduciaries to document:

- fee limits

- liquidity standards

- valuation methodologies

- conflict disclosures

- prohibited transaction reviews

- insurance credit standards

they often contain broad statements about “diversification,” “prudent investing,” or “appropriate alternative investments.”

An IPS that avoids measurable standards protects fiduciaries far better than it protects participants.

That is not an accident.

Governance Theater

One of the CFA paper’s best observations is that many investment committees have become governance rituals rather than genuine decision-making bodies. Meetings are held. Minutes are written. Consensus is achieved. This is 99% of committee meetings.

As a Kentucky Pension trustee of a $20 billion fund, I would make written objections to investment decisions around a lack of transparency to be entered into the minutes, after I found them scrubbed from previous minutes. The rest of the board then voted to scrub my written comments from the minutes. I the only investment expert of 12 was removed from the investment committee led by a trustee who later served a 5 year prison term.

Committees now often perform diligence around information that has already been filtered by consultants, investment managers, placement agents, legal counsel, and proprietary confidentiality agreements.

Trustees are frequently asked to approve billion-dollar commitments after seeing only a fraction of the relevant information. The meeting itself becomes evidence that a prudent process occurred—even when the most important information was never available.

The Elephant in the Committee Room

Perhaps the most surprising omission in the CFA monograph is private equity.

Today, alternatives dominate institutional investing.

Yet there is remarkably little discussion of:

- opaque valuations

- carried interest

- subscription credit facilities

- secondary market discounts

- side letters

- manager conflicts

- performance reporting differences

- benchmark selection

These are no longer niche issues. They define modern institutional governance.

From Behavioral Finance to Fiduciary Finance

The CFA Institute has made an important contribution. It explains how committees think. The next generation of research must explain what committees are obligated to investigate. Those are very different questions. Behavioral finance asks: How do groups make better decisions?

Modern fiduciary governance asks: What information must fiduciaries obtain before any prudent decision is even possible? That distinction increasingly defines pension governance.

The Next Generation of Governance

The next major advance in committee governance will not come from better meeting procedures.

It will come from requiring committees to document objective fiduciary standards before investments are approved.

Future Investment Policy Statements should require documented analysis of:

- total fees from every source

- valuation methodology

- secondary market evidence

- liquidity stress testing

- conflicts of interest

- prohibited transaction analysis

- insurance credit risk

- benchmark selection

- GIPS compliance where applicable

- independent verification of reported returns

Those questions matter far more than who speaks first during committee meetings.

Conclusion

The CFA Institute deserves credit for improving the science of investment committee behavior. But today’s governance crisis is no longer primarily behavioral. It is informational.

When trustees knowingly approve billions of dollars in investments whose valuations, fees, contracts, and risks remain largely hidden, the problem is not groupthink. It is fiduciary blindness. The greatest governance reform of the next decade will not be quieter committee meetings or anonymous portfolio voting.

It will be restoring the simple principle that fiduciaries cannot prudently approve what they are not allowed—or unwilling—to fully examine.

Love both posts, but what’s the basis for the claim that investment committees are smarter than ever? Seems to me they are worse informed than ever, as you mentioned. I agree with your premise that more often than not, they just go through the procedural motions due to issues such as transparency.

I will mention this post in one my posts in my current series of posts on integrating AI into plan design and monitoring, my overall thesis being that AI arguably raises the “should have known” standard under 404(a).

Yahoo Mail: Search, Organize, Conquer

LikeLike