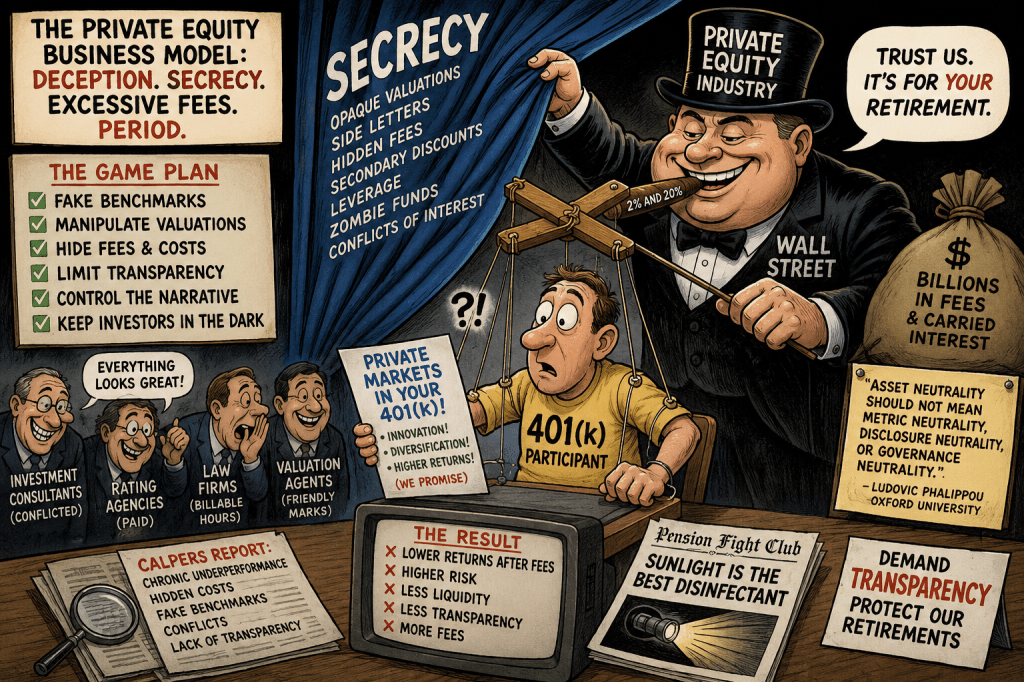

The private equity industry does not merely prefer secrecy.

It requires secrecy.

Without opaque valuations, manipulated benchmarks, hidden fees, and misleading performance metrics, the industry’s excessive fee structure could not survive in a competitive marketplace.

That is the uncomfortable truth at the center of the Department of Labor’s proposal to open 401(k) plans to private equity products. And after reviewing more than 40,000 public comments submitted to the DOL, none stands out more than the analysis submitted by Professor Ludovic Phalippou of Oxford University — arguably the world’s leading academic expert on private equity performance and valuation.

The industry’s defenders talk endlessly about “innovation,” “access,” and “democratization.”

Ludo talks about math.

And the math is devastating. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=6847259

As Phalippou explains in his formal DOL submission, the private equity industry’s favorite performance metric — Internal Rate of Return (IRR) — is not actually a measure of investor wealth compounding at all. It is a discount-rate formula that can be heavily manipulated through timing, subscription lines, dividend recaps, and cash-flow engineering.

In plain English: private equity markets returns in a way that would never be tolerated in public mutual funds.

Phalippou demolishes the fantasy using the industry’s own numbers.

KKR has reported roughly 26% since-inception IRRs for almost twenty years straight. Apollo has reported approximately 39% since-inception private equity IRRs for decades. If those numbers reflected actual investor wealth compounding, Apollo’s original funds would theoretically be worth sums approaching the GDP of the United States.

That is not investing.

That is marketing arithmetic.

Phalippou’s central point is simple but devastating:

“Asset neutrality should not mean metric neutrality, disclosure neutrality, or governance neutrality.”

The private equity industry survives because it is allowed to compare apples to oranges while charging exponentially higher fees than transparent public markets.

And that deception is spreading.

The Entire Business Model Depends on Preventing Transparency

If private equity managers were forced to:

- disclose all fees like SEC mutual funds,

- use public-market-equivalent benchmarks,

- fully report portfolio-company fees,

- mark assets honestly,

- disclose secondary-sale discounts,

- reveal side letters,

- and compare performance against low-cost index funds,

the economics of the industry would collapse.

That is why transparency itself has become the industry’s existential threat.

The recently released independent forensic CalPERS investigation highlights exactly how this system operates inside the nation’s largest public pension.

The report documents:

- chronic underperformance,

- hidden and understated investment costs,

- fake “custom” benchmarks,

- consultant conflicts,

- opaque valuations,

- zombie private-equity funds,

- and aggressive resistance to transparency.

The report’s findings are extraordinary because CalPERS is not some small fringe pension.

CalPERS is the herd leader. https://www.rpea.com/view/download.php/news/calpers-investigation-report

When CalPERS normalizes secrecy, benchmark manipulation, and opaque alternatives, other pensions follow.

As the report explains:

“Investors globally are harmed when the pension leader misleads.”

Fake Benchmarks Create Artificial Alpha

One of the most important findings in the CalPERS investigation is that private equity underperformance is hidden through benchmark engineering.

CalPERS uses non-investable “custom benchmarks” like:

- CPI + 400 basis points,

- FTSE All-World + 150 basis points,

- or internally constructed composite benchmarks.

These are not real portfolios that investors can buy.

They are fictional scoreboards designed to be beaten.

The report correctly calls this “Artificial Alpha.”

Richard Ennis famously described the process as “chasing slow rabbits.”

The game works like this:

- Create a benchmark nobody can actually invest in.

- Compare private assets to that benchmark.

- Ignore hidden leverage, stale valuations, and illiquidity.

- Claim outperformance.

- Justify higher fees and bonuses.

Meanwhile, simple transparent index funds often outperform after fees.

That is precisely why the Supreme Court’s Intel case matters so much.

As discussed previously in The Supreme Court’s Intel Case Is About Secrecy, Fake Benchmarks and Fiduciary Illusions, the private markets industry depends on preventing participants from seeing what meaningful comparisons would actually reveal. https://commonsense401kproject.com/2026/01/17/the-supreme-courts-intel-case-is-about-secrecy-fake-benchmarks-and-fiduciary-illusions/

Because once participants compare:

- true fees,

- true liquidity risk,

- true valuations,

- and true after-fee performance

against low-cost public alternatives, the illusion breaks down.

The Industry Knows Transparency Is the Real Threat

The most revealing quote in the entire CalPERS investigation may be this statement from CalPERS CEO Marcie Frost on CNBC:

“CalPERS is not sharing the limited partnership agreements. CalPERS is not sharing any side letters… We are extremely transparent… But frankly, private markets are private for a reason…”

That single sentence captures the entire private-equity model.

Private markets are “private” because transparency threatens fees.

The secrecy protects:

- side-letter arrangements,

- valuation games,

- portfolio-company fees,

- subscription-line engineering,

- fee layering,

- secondary-sale discounts,

- political relationships,

- and benchmark manipulation.

The industry cannot tolerate sunlight because sunlight would expose how much of private equity’s reported “alpha” comes from:

- stale marks,

- leverage,

- fee extraction,

- and benchmark engineering.

“Pension Fight Club” Exposes the Fear

The movie Pension Fight Club captures something the industry desperately wants to avoid: ordinary retirees beginning to ask questions.

The film repeatedly focuses on:

- secrecy,

- intimidation,

- missing records,

- hidden fees,

- consultant conflicts,

- and retaliation against pension critics.

One recurring theme is that pension beneficiaries are treated as adversaries once they demand transparency. Free trailer at https://pensionfightclub.com/ low fee for full movie.

That aligns perfectly with the findings of the CalPERS investigation, which documented coordinated efforts by pension officials and industry allies to undermine participant scrutiny and participant-funded investigations.

The message from the industry is clear:

Participants may fund the system.

But they are not supposed to understand the system.

The DOL’s Proposed Rule Is a Gift to Wall Street

The DOL claims its proposal is “asset neutral.”

But there is no such thing as neutrality when one side:

- hides fees,

- manipulates benchmarks,

- controls valuations,

- limits disclosure,

- restricts liquidity,

- and markets misleading performance metrics.

As Phalippou warns, allowing private equity into participant-directed retirement plans without strict disclosure and benchmarking rules does not reduce risk.

It merely transfers the risk to retirement savers.

The irony is overwhelming.

ERISA imposed strict disclosure rules on mutual funds precisely because regulators recognized that retirement savers could not evaluate opaque products.

Now the DOL proposes opening 401(k)s to products far more opaque than anything ERISA originally allowed.

This is not modernization.

It is deregulation for Wall Street’s most secretive and highest-fee industry.

The Core Problem Is Not Complexity — It Is Incentives

Private equity defenders constantly argue that critics simply “do not understand” sophisticated investments.

That is false.

The issue is not complexity.

The issue is incentives.

The industry earns dramatically higher fees when:

- valuations are opaque,

- benchmarks are fictional,

- costs are hidden,

- and comparisons are impossible.

Transparency threatens the economics of the business itself.

That is why private equity fights:

- public records requests,

- disclosure reform,

- benchmark standardization,

- independent valuation review,

- and participant oversight.

If private equity truly delivered superior risk-adjusted returns after all fees and expenses, transparency would help the industry.

Instead, the industry treats transparency as an existential danger.

That tells you everything you need to know.

https://commonsense401kproject.com/2026/05/04/the-diversification-lie-how-private-equity-and-private-credit-use-corrupt-accounting-to-hijack-pension-and-401k-allocations/https://commonsense401kproject.com/2025/10/27/private-equity-as-an-erisa-prohibited-transaction/

“Participants may fund the system. But they are not supposed to understand the system.”

Yahoo Mail: Search, Organize, Conquer

LikeLike